- sagunreadymadeudhyog@gmail.com

- Goghapulchowk, Buddha Marg, Biratnagar-9, Nepal

Search for anything..

An Overview of Textile and Apparel Industry of India & China

An Overview of Textile and Apparel Industry of India & China

In terms of Textile and Apparel, India and China are two major producing and manufacturing giants who play a vital role in determining the global economic dynamics. With mass production and manufacturing capabilities, both these nations share the potential to increase as well as influence the global economy.

Nepal Export and Import |Apparel and Textile

According to the Nepal Foreign Trade Statistics For The Fiscal Year (2076/77), Ready-made garment (RMG) is one of Nepal’s top 10 Imported commodities. Nepal has imported RMG with a value of staggering NPR. 54.52 billion generating a total revenue of NPR.18.14 billion in the fiscal years (2075/76 and 2076/77) collectively.

When we talk about RMG and textile sectors, Nepal is far behind the Global players. However, Nepal certainly shares borders with two global leaders in the Apparel and Textile industry i.e India and China.

Understanding the dynamics of China’s and India’s RMG and Textile Supply Chain is a must as both are Nepal’s major trade partners in this sector.

In today’s blog, we will analyze the textile and apparel industries of India and China. Sharing with you the competitiveness of the textile and clothing supply chain of two nations is the key objective of this blog.

Let us briefly look into the vulnerability index of India and China in the Clothing and Textile sectors.

Vulnerability Index in Clothing and Textile Sector | India and China

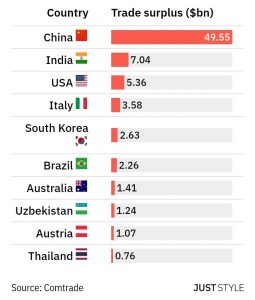

As a matter of fact, A study was conducted recently by Just Style. It analyzed data provided by the global trade database Comtrade. The study aimed to determine which countries’ apparel and textile industry are least vulnerable by exploring the balance between

- Apparel Import & Export

- Textile Import & Export

Let’s take a look at some of the statistics

India

India exported apparel worth $18.91 billion in 2020 while importing $1.93 billion resulting in a $16.98 billion goods surplus.

Similarly, India exported $10.65 billion in textile raw materials while importing only $3.61 billion resulting in a $7.04 billion in goods surplus. In a nutshell, the apparel and textile industry collectively contributed a $24.02 billion surplus which is almost 5 times the import. i.e (Import-Export) ratio of (1:5)

China

China exported finished apparel worth $238.33 billion in 2020 while importing $15.66 billion resulting in a whopping $222.67 billion in goods surplus.

Similarly, China exported $70.61 billion in textile raw materials while importing $21.05 billion resulting in a $49.55 billion goods surplus. The apparel and textile industry collectively contributed a $272.22 billion surplus which is almost 7.5 times the import. (Import-Export) the ratio of (1: 7.5)

Direction of Trade

India and China both show a similar pattern as both economies are trending high in apparel and textile supply chains when it comes to resiliency and vulnerability.

- China ranked highest in both indices i.e. (‘least vulnerable in textile supply chain’ and ‘least vulnerable in the apparel supply chain’)

- India was listed in the top three in both indices. i.e. (‘least vulnerable in the textile supply chain’ and ‘least vulnerable in the apparel supply chain’)

There is a substantial gap in terms of volume with China leading. However, it is interesting to note that the Indian textile Industry is emerging quite competitive in terms of production rate.

Now, let us take a look at recent developments in China’s Supply Chain Strategy which have direct implications for RMG and Textile Sectors.

“China’s Plus One” Supply Chain Strategy and its Implication in RMG and the textile industry

China’s Plus One is the business strategy to avoid investing only in China and diversify the business into other countries.

The Plus One strategy was specifically triggered by the global COVID-19 pandemic. As part of its strategy, China has been prioritizing manufacturing high-value goods instead of low-value goods.

Why would China do so?

Western businesses have been making investments in China over the past 20 years. They were attracted by the country’s low production costs and sizable domestic consumer markets.

However, the advantages of the cheap labor & market demand that China initially provided have been overshadowed by ASEAN and SAARC countries. Countries like Vietnam, the Philippines, Thailand, Bangladesh, and India have been providing similar advantages.

Furthermore, with increasing labor wages in China, the cost of doing business increased, especially among RMG and textile manufacturers. Some analysts suggest that the long-term stability and safety area is a major reason for this strategic change by China.

What does it Imply?

With the shift in the manufacturing supply chain, the plus one strategy is likely to create opportunities for Indian Manufacturers, especially in the apparel and textile industry.

With China shifting from Cost-driven to Innovative-driven manufacturing, manufacturers are expected to focus on their fast-growing domestic market. This would reduce its global share and create an export market vacuum of around $50 billion by 2025. (as per FICCI)

Several Multinational corporations have been looking at countries like India, Vietnam, Indonesia, Malaysia, Thailand, the Philippines, and Bangladesh.

What it means to India?

UnlikeIndia, China does not have enough supply of cotton yarn, discouraging some local giants to invest further in this space. In fact, Part of this scarcity is what led to Chinese manufacturers’ growing interest in man-made fibers.

India has the second-largest manufacturing industry and is also the second-largest cotton producer after China.

In India, this opportunity could lead to additional demand and additional CAPEX to tune into gains of Rs 120 billion over the next 10 years.

The Indian government has increased its attention and investments in ramping up its textile production and export business. The government is providing lucrative incentive schemes to manufacturers of fabrics and apparel in the artificial fiber segment and domestic technical textile firms.

In Sep 2021, the Union Government approved the Production-Linked Incentive (PLI) Scheme for Textiles products. The government has approved a financial outlay of Rs 10,683 crore for five-year to enhance India’s manufacturing capabilities and exports.

Conclusion

One of key takeaways from both economies is that though the manufacturing of clothes seems lucrative in countries with low labor costs, it is not the only factor that determines success.

In fact, it is production efficiency with sufficient product differentiations that serves as the biggest profitability factor apparel and textile industry.

Two of our neighboring nations submerged in globalization have made immense progress in the apparel and textile manufacturing sector.

It would be a fair statement to make that China and India both strategizing to modify their supply chain, are going to be key players in determining the textile and garments trends in southeast Asia. Especially for Nepal which happens to be in between two manufacturing giants with both nations being the major importing partners.

Also Read: Top 10 Questions to ask your Potential Ready-made garment manufacturer

Sagun Readymade Udyog

The garments which are available in our shop are for different age groups with varied color combinations, up to date styles, latest prints, and trims and also suitable for different occasions and seasons.